An Unpredictable Start to the Year

If there’s one word to define the first quarter of 2025, it’s volatility. Since January, we’ve seen President Trump and his administration swiftly roll out a sweeping policy agenda that’s shifting the trajectory of domestic and global markets. Aggressive tariffs on key trading partners represent a stark pivot from decades of global economic integration. Simultaneously, government spending cuts headed by the Department of Government Efficiency (DOGE) have some economists warning that these mass layoffs could alone push the economy into recession.

The uncertainty accompanying these changes has rippled across financial markets. Equities, bonds, and interest rates have all experienced dramatic downswings in value only to recover sharply days or weeks later. With so many mixed signals, some analysts began the year forecasting growth and then changed to expecting a recession and deep market corrections, only to reverse course again, calling for continued growth. These rapid changes have increased uncertainty across the board, making future earnings and stock market valuations particularly difficult to assess.

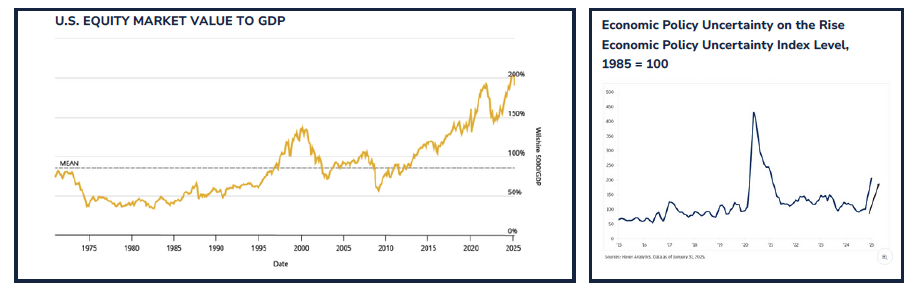

Warren Buffett’s actions provide a telling signal for prudent investment in this environment. In Q1 2025, Berkshire Hathaway continued its defensive stance, marking its tenth straight quarter as a net seller of equities. The company’s cash reserves now exceed $348 billion. Meanwhile, the famed Buffett Indicator, which compares the total market cap of publicly traded U.S. stocks to GDP, is nearing an all-time high of 200%.

Alternatives in Focus: A Growing Share of the Investment Landscape

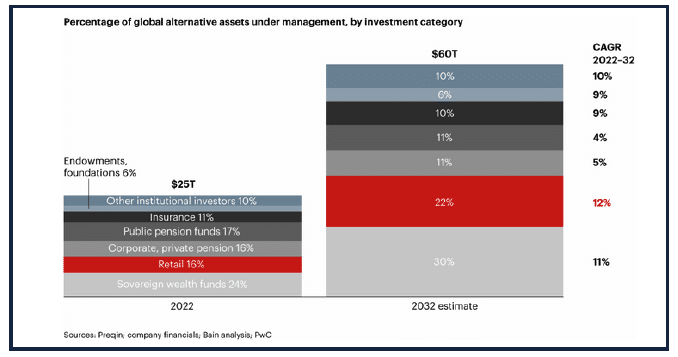

While headlines focus on public markets, alternative investments are quietly growing in both scale and importance. In 2002, global alternatives accounted for $2 trillion, just 5% of global investment assets. Today, that figure exceeds $25 trillion, or 15% of the now $150 trillion global investment market. Forecasts show that its trajectory will continue and Bain projects that by 2032, alternatives will surpass $60 trillion, with retail investors representing 22% of that growth.

Strategically implemented, alternatives can help smooth portfolio performance in times of market turmoil. Alternatives typically value the underlying investments on a much longer-term outlook than publicly traded assets, shielding investors from the daily price swings we have become so accustomed to seeing this year. Investors who are focused on long-term value creation have continued to see this as an attractive hedge in their portfolio. In Larry Fink’s (CEO of Blackrock) annual letter to investors, Fink wrote “The future standard portfolio may look more like 50/30/20 stocks, bonds, and private assets like real estate, infrastructure, and private credit… Generations of investors have done well following this (the 60/40) approach, But as the global financial system continues to evolve, the classic 60/40 portfolio may no longer fully represent true diversification.”

For investors, this means that vast amounts of new capital will be pursuing assets in areas that have traditionally had more limited sources of investment. This additional demand surging into a market with supply constraints like private real estate means higher valuations for those holding these precious investment opportunities that the new capital seeks.

Office: Fragmented Market, Focused Opportunities

Despite broad headlines declaring office space oversupplied and stagnant, we are seeing real opportunity, if you know where to look.

With the outlook of a sharp decline in interest rates no longer a realistic possibility, we are seeing institutional owners begin to completely exit their office investments. This is particularly true in secondary markets and a decision that is driven by top-down boardroom mandates rather than market-specific fundamentals. While grounded in the reality that office properties in general continue to face real challenges, it ignores the nuance that some properties have extreme difficulty while others are experiencing near-record demand. The general market sentiment about office properties means that very few investors are purchasing them, and even those with very strong demand are receiving pricing like that of their distressed peers. We are being very diligent and selective in our underwriting, but opportunities in this space are increasingly compelling.

In this environment, quality is the dividing line between the haves and have-nots in office assets. Tenants continue to demand A+ locations, A+ product, and A+ amenities, and they’re willing to pay for it. As employers push return-to-office mandates and the labor market remains tight, prime buildings are outperforming the broader market.

The first quarter of 2025 marked the fourth consecutive quarter where leasing activity has outpaced vacancies. When comparing this quarter’s leasing velocity to the same period last year, we see an 18% year-over-year increase. This momentum is being fueled by prime office space, which accounted for over 2 million square feet of leases during the quarter, resulting in a prime vacancy rate of 14.8%, nearly 4.2% below the broader office average.

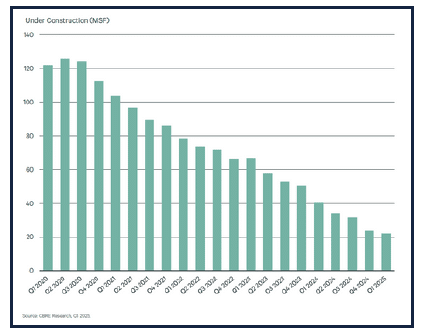

Meanwhile, a thinning construction pipeline is creating scarcity in best-in-class assets. Completions are expected to total just 15 million SF this year, the lowest annual figure since 2012. This decrease in new construction will make it more challenging for tenants to find prime office space, but it should positively impact existing office inventory and help stabilize the overall vacancy rate.

Industrial: Demand Shifts and a Path to Stabilization

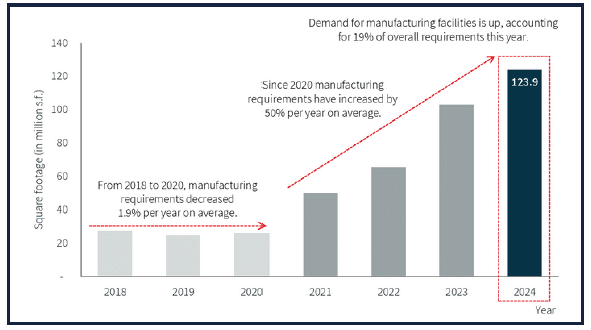

In the industrial sector, both short-term and long-term trends continue to evolve as companies navigate global uncertainty and reposition supply chains for resilience. Organizations are diversifying suppliers, reshoring operations, and investing accordingly. These macro shifts are supporting an increase in demand for modern manufacturing space. According to JLL’s most recent quarterly outlook, they project that future manufacturing demand will account for close to 19% share of the total industrial demand, marking a 354% increase since 2018. This is a result of companies optimizing their production processes and bringing operations closer to retail customers.

On the supply side, the new construction pipeline is finally cooling. After 11 quarters where new deliveries outpaced absorption, completions are now falling below pre-pandemic levels. This is evident in the slowing of the vacancy rate. During the first quarter, vacancies rose by just 14 basis points, which was the smallest increase since the fourth quarter of 2022. By late 2025, forecasts are now projecting the vacancy rate to stabilize as the supply-demand gap narrows.

With the vacancy rate approaching stabilization, we are seeing rents continue to rise in most regions. During the quarter, we saw the average weighted rent increase 3% year over year, up to $11.05 SF NNN. In the warehouse and distribution sector, we saw rents increase 6% year-over-year.

Tax and Regulation Changes

It’s almost certain that major changes in taxes will come about this year. With the original tax cuts from the first Trump administration set to sunset this year, the pressure is on Congress to deliver a new tax bill. In the past few days, the draft of the house budget resolution titled “The One Big Beautiful Bill” was released.

While much wrangling remains before the bill even receives a floor vote, it seems likely that it will pass the House and Senate in some form in the coming months. The draft bill contains several provisions that would enhance the economic value of real estate investments, including a reduction in the effective tax rate for distributions such as those from Tempus Evergreen, enhanced ability to realize the tax benefit of depreciation sooner, and major new incentives for building and expanding manufacturing properties.

Evergreen Portfolio Update: Continued Outperformance

During the first quarter of 2025, we received our finalized year-end valuation from Ernst & Young, which reflected an increase in property values and Evergreen’s share price. As a result, Evergreen’s life-to-date annualized net return has reached 10.7%, significantly outperforming industry benchmarks NCREIF and NAREIT, as well as Blackstone BREIT, Nuveen GCREIT, Starwood SREIT, and ARES REIT.

We are excited about the results and continue to explore opportunities to add properties to Evergreen, thereby bringing additional diversification. In the second quarter, Evergreen will be investing in flagship property located in Pittsburgh, PA. This asset exemplifies the Evergreen standard of best-in-class location, amenities, and quality. In addition, Tempus has officially broken ground on the new corporate headquarters for Montrose Environmental Group (MEG). Upon completion, this property will be added to the Evergreen portfolio.

Final Thoughts: Staying Disciplined

Despite the first quarter of 2025’s volatility, our strategy remains steady: investing in high quality real estate, maintaining conservative capital structures, and creating long-term value. Staying selective, focused, and disciplined amid volatility is not just a wise strategy; it’s a skill that requires foresight and composure, but for those who do so consistently, it becomes a competitive advantage.